Gold, silver pull back on profit taking and as USDX rebounds

Gold prices are lower and silver well down from its daily high in midday U.S. trading Thursday. Profit taking from the shorter-term futures traders is featured in both metals after gold hit a nine-month high and silver a four-week high overnight. A rebound in the U.S. dollar index today after its pounding Wednesday is also a bearish daily outside market element for the precious metals. Still, both gold and silver are in firm near-term technical control. April gold was last down $10.10 at $1,932.70 and March silver was up $0.036 at $23.65.

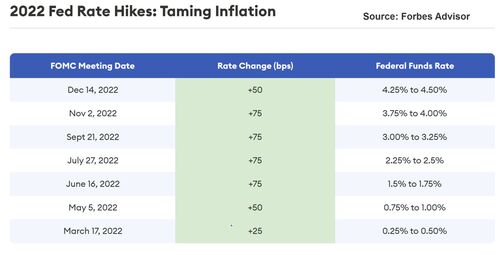

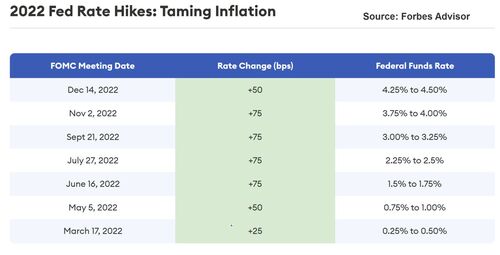

The marketplace Thursday was still digesting Wednesday afternoon's FOMC statement and Fed Chair Jerome Powell's press conference. The Fed raised the Fed funds rate range by 0.25%, as widely expected. However, Powell's remarks at his presser led the marketplace to believe the Fed is close to ending its string of interest rate increases. Powell said inflation is receding but needs to pull back farther. He mentioned the word "disinflation" as characterizing the present U.S. economic conditions. Most agreed that in the final assessment, Powell was not nearly as hawkish as he had been in recent FOMC press conferences and left the door open to a Fed "pivot" sooner rather than later.

Gold price gains as Fed Chair Powell talks disinflation but warns it's too early to declare victory

Today was the regular monetary policy meetings of the European Central Bank and the Bank of England, which saw both central banks raise their main interest rates by 0.5%. The moves were not unexpected.

Focus now turns to Friday morning's January U.S. employment situation report from the Labor Department. The key non-farm payrolls number is expected to be up 187,000 jobs, following a rise of 223,000 in the December report.

The key outside markets today see the U.S. dollar index higher but it hit a nine-month low overnight. Nymex crude oil futures prices are a bit firmer and trading around $76.50 a barrel. Meantime, the yield on the benchmark U.S. 10-year Treasury note is presently fetching 3.365%.

.gif)

Technically, April gold futures prices hit a nine-month high early on today and then reversed course to score a bearish "outside day" down on the daily bar chart. Bulls still have the solid overall near-term technical advantage. A three-month-old uptrend is in place on the daily bar chart. Bulls' next upside price objective is to produce a close above solid resistance at $2,000.00. Bears' next near-term downside price objective is pushing futures prices below solid technical support at $1,900.00. First resistance is seen at $1,950.00 and then at today's high of $1,975.20. First support is seen at $1,925.00 and then at this week's low of $1,915.50. Wyckoff's Market Rating: 8.0

March silver futures prices hit a four-week high early on today. The silver bulls have the overall near-term technical advantage. However, trading has been choppy and sideways at higher levels. Silver bulls' next upside price objective is closing prices above solid technical resistance at the January high of $24.775. The next downside price objective for the bears is closing prices below solid support at $22.00. First resistance is seen at $24.00 and then at last week's high of $24.415. Next support is seen at this week's low of $23.05 and then at the January low of $22.845. Wyckoff's Market Rating: 6.5.

March N.Y. copper closed down 35 points at 410.75 cents today. Prices closed near the session low and hit a three-week low today. The copper bulls have the firm overall near-term technical advantage but are fading a bit. A four-month-old uptrend on the daily bar chart has stalled out. Copper bulls' next upside price objective is pushing and closing prices above solid technical resistance at the January high of 435.50 cents. The next downside price objective for the bears is closing prices below solid technical support at 395.00 cents. First resistance is seen at 420.00 cents and then at this week's high of 424.90 cents. First support is seen at this week's low of 410.25 cents and then at 405.00 cents. Wyckoff's Market Rating: 7.0.

By Jim Wyckoff

For Kitco News

David

LBMA annual survey sees gold prices averaging the year around $1,859 an ounce, silver to hold around $23.65

LBMA annual survey sees gold prices averaging the year around $1,859 an ounce, silver to hold around $23.65

Gold is vulnerable to a pullback as Powell prepares to signal 'seriousness', but will hit an all-time high in 2023 – Adrian Day

Gold is vulnerable to a pullback as Powell prepares to signal 'seriousness', but will hit an all-time high in 2023 – Adrian Day

Stock markets are set to crash 37% as 'sucker's rally' ends, gold and silver to 'take off' – Chris Vermeulen

Stock markets are set to crash 37% as 'sucker's rally' ends, gold and silver to 'take off' – Chris Vermeulen

.jpg)