Waterfall decline in gold induces miner capitulation

The headwinds from persistent strength in the U.S. dollar and 10-year bond yields moving closer to 5% have proved too much for the gold market as prices have fallen to their lowest level since March. Gold lost key support at $1900 in September, when the month and quarter ended last Friday. With the Chinese market being closed during "Golden Week," Western bullion banks were primed to continue covering short positions into October during a waterfall decline in Gold Futures down towards its rising 200-week moving average at $1820.

Yet, once you step back to look at the bigger macro picture that is currently unfolding, it is not hard to see that the stars are aligning for gold. Although the bears have been able to break through the six-month gold floor at $1900, rising energy prices coupled with slower economic growth are creating a stagflationary environment which will eventually push Gold Futures back above $2000 an ounce.

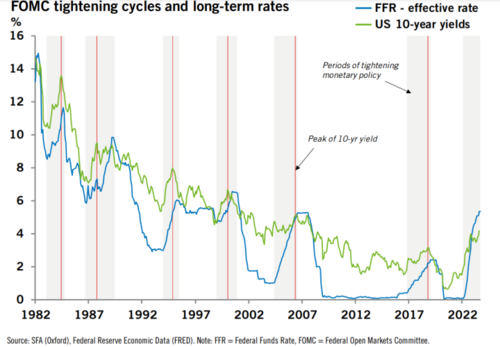

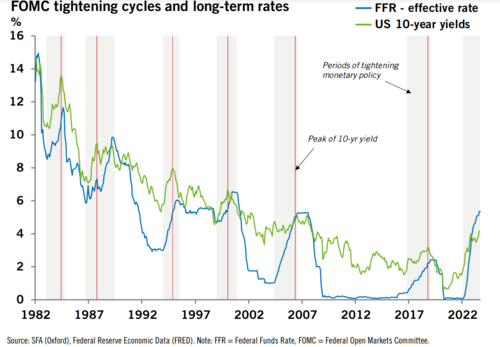

As we transition through the final quarter of 2023, the list of known risk factors is expanding as an unrelenting selloff in government bonds has sent global treasury yields to levels last seen prior to the Global Financial Crisis in 2008. Government borrowing costs influence everything from mortgage rates for homeowners to loan rates for companies.

Rising debt and geopolitical instability could also make U.S. bonds less attractive to foreign investors. The risk now is that the Federal Reserve loses control of yields and is forced to be a buyer of last resort. If yields continue to climb, the world's most powerful central bank may be forced to increase its balance sheet with new quantitative easing measures before cutting rates. Not to mention the Fed publicly giving up on its fantasy of getting back to 2% inflation, which would be a major positive for the gold price.

The speed of the bond rout has spooked stock investors as well, with all major equity indexes wiping out their gains for the year. The S&P 500 erased all its gains for 2023 and tumbled into correction territory this week. Some analysts have compared the strong run-up in stocks in 2023 to the price action leading up to the 1987 crash.

In 1987, the S&P 500 rallied about 39%, peaked in August, the crashed in October to erase all its gains in just two weeks. The current rally that started in October 2022 gained about 31% into July, and is now setting up a potential panic move lower. If the S&P 500 closes below critical support at 4200 later today, the odds of a waterfall decline during crash season would increase significantly.

The gold price has been incredibly resilient in the face of skyrocketing bond yields. The 10-year bond rate was around 2.5% a year ago, and gold was trading around $1820. Now, after rates have nearly doubled up to 4.8%, gold is still trading at $1820 as Eastern central banks continue to add more bullion to their reserves.

According to the latest data from the World Gold Council this week, central banks bought 77 tonnes of gold in August, a 38% increase compared to buying in July. Over the last three months, central banks have bought 219 tonnes of gold. This comes after record purchases during the first half of the year.

The continued buying shows central bank gold demand is far from being saturated. The U.S. dollar's persistent strength means that nations with U.S. dollar-denominated debt continue to face high financing costs. The only way to reduce those costs is to diversify away from the U.S. dollar and gold remains the most attractive global monetary asset.

As 10-year bond yields move closer to 5%, Western investors may be close to waking up to the growing debt risks in the U.S. Once Western investors begin to become more defensive as recession fears grow, we will start to see investment demand for gold pick up.

Most economists have felt over the past several months that the Federal Reserve has gone one rate hike too far. And with the odds increasing of another rate hike coming next month, the biggest risk is that the Fed may commit yet another policy error after insisting inflation was "transitory" for a year before beginning to hike rates in March 2022.

By waiting far too long before hiking rates as inflation raged, the Fed has boxed itself into a corner after raising rates at its fastest pace in over 40 years – while government eliminated the debt ceiling. The further the central bank goes into restrictive territory, the more likely it becomes that we begin to see black swan events – just like we saw recently with the second, third and fourth largest bank failures in U.S. history.

If the Fed pushes too hard on rates, the 10-year could spike above 5% and this would raise the odds of breaking something in the financial system. The regional banking crisis in March sparked an over $250 move higher in the gold price from levels it has come back to test this week. But if the central bank stands pat, back-to-back pauses would support an end to the tightening cycle, which would also be bullish for gold.

The U,S, ADP report this week revealed a twelfth straight weekly decline in wages on a debt-saddled population. We should expect to see further volatility and uncertainty in the U.S. dollar as the country's government debt continues to grow along with its citizenry.

Consumer credit card balances and personal interest payments are soaring. U.S. credit card balances crossed the $1 trillion mark this summer as more Americans turned to debt to fund their everyday needs. With interest on credit cards now over 22% the average debt-laden consumer is getting crushed, resulting in delinquencies also climbing as that strategy becomes increasingly untenable.

U.S. debt is approaching $33.5 trillion. At the same time, the deficit is on pace to increase by $2 trillion this year. The eventual economic consequences of the burgeoning government debt include slower growth as more resources get used and allocated by the government.

A likely monetary consequence is that regardless of what senior members of the Fed currently say and think (they naturally insist that the Fed is independent), there is a high probability that the Fed eventually will yet again be called upon to help finance the government.

Historically, the biggest positive for the gold price has been loss of confidence in Fed policy and government. The looming U.S. government shutdown may still be a catalyst for gold even after the current crisis has been pushed out for 45 days.

A split Congress is at loggerheads yet again over government funding just as U.S. bond markets are pricing the most expensive Treasury borrowing in 16 years – while also rethinking the long-term trajectory for interest rates and fiscal policy.

A near-miss on a debt ceiling showdown in the Spring led to the loss of another Triple-A sovereign credit rating, followed by further brinkmanship over next year's spending bills. According to a recent warning from Moody's, the dysfunction in public financing and potential for debt servicing disruption may threaten the last remaining AAA credit rating of the main three agencies.

Furthermore, the U.S. House of Representatives for the first time in its history has booted its speaker out of the job, as infighting in the narrow and bitterly divided Republican majority toppled Kevin McCarthy from the position. This unprecedented action now creates a political crisis, plunging the House of Representatives into inevitable confusion and uncertainty, not to mention a highly contentious battle over the speaker position.

Until a House speaker is installed, it is unlikely that further action will be taken on bills to fund the government, with lawmakers facing a Nov. 17 deadline to provide more money or face a partial government shutdown. Republican lawmakers said they would need at least a week to choose a new speaker, which will eat into the time necessary to pass that needed legislation.

This dilemma coincides with Republicans simultaneously battling the calendar to complete the appropriations process and continues its impeachment investigation into President Joe Biden.

Meanwhile, gold stocks are presenting the best risk/reward situation we have seen since late 2015 after Gold Futures have now printed nine consecutive daily red candles to become deeply oversold. Both GDX and GDXJ are testing the lower boundary of their respective downtrend channels as a final capitulation by worn out gold stock investors takes place.

A similar correction pattern amid sector capitulation occurred into the second week of 2016. The exact low back then came in the form of an intra-day bear-trap reversal to the upside, which took many bottom-fishers accumulating quality juniors since early Q4 2015 quickly out of position.

There was no major news to trigger the event, it was just the algorithm switch being flipped after a similar capitulation had run its course. And those investors who sold were left to watch many of the juniors they capitulated go 5-10x higher in just six months, while refusing to buy them back at higher prices along the way after being burned.

In anticipation of the incredible gains the junior sector should begin to experience once the gold price prints a technical breakout above $2100, the Junior Miner Junky (JMJ) newsletter has accumulated a basket of quality juniors with 3x-10x upside potential into 2025-26.

If you require assistance in accumulating the best in breed precious metals related juniors, and would like to receive my research, newsletter, portfolio, watch list, and trade alerts, please click here for instant access.

By

David Erfle

Contributing to kitco.com

David

Bond yields can't keep gold down forever as ING sees higher prices in 2024

Bond yields can't keep gold down forever as ING sees higher prices in 2024

Central banks buy 77 tonnes of gold, helping the precious metal resist rising bond yields

Central banks buy 77 tonnes of gold, helping the precious metal resist rising bond yields

Nervous crypto investors gain comfort via total return approach instead of only chasing price gains

Nervous crypto investors gain comfort via total return approach instead of only chasing price gains

The Fed to hike rates again in November, rate cuts coming only in 2025, here's why – Pat LaVecchia

The Fed to hike rates again in November, rate cuts coming only in 2025, here's why – Pat LaVecchia