LME metals rebound after Friday’s correction, but prices weaker in Shanghai

The broader markets were mixed on the morning of Monday February 10, with equities in Asia generally weaker, as were metals on the Shanghai Futures Exchange, while the London Metal Exchange was firmer across the board.

There is still much uncertainty around the impact of the Wuhan coronavirus (2019-nCoV), but with more businesses returning to work in China this week, we might get a better feel for the likely impact on Chinese demand.

With China generally a net importer of metals, the demand shock could well see inventories build up in the country and along the supply chains that supply China, while exports of products are also likely to continue to be disrupted.

China’s CSI 300 is up by 0.21%, while other Asian equity indices are lower

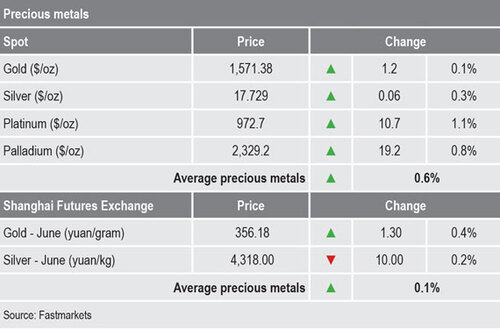

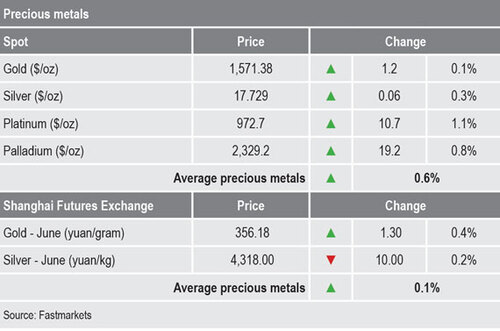

Gold prices are edging higher again, recently quoted at $1,571.40 per oz

Base metals

Three-month base metals prices on the London Metal Exchange were up by an average of 0.9% this morning, but this is after an average fall of 1.9% on Friday. Nickel led the gains this morning, with a 1.4% rise to $13,005 per tonne, followed by a 1.3% rise in tin to $16,500 per tonne, while copper is up 0.9% at $5,704 per tonne.

Trading volumes have been above average again with 9,871 lots traded as of 5.37am London time.

In China, the most-traded base metals contracts on the Shanghai Futures Exchange were, for the most part, weaker and down by an average of 0.4%, with April aluminium the only metal bucking the trend with a 0.1% gain, while April zinc led on the downside with a 1% fall. April copper was off 0.4% at 45,650 yuan ($6,532) per tonne.

The spot copper price in Changjiang was down by 0.6% at 45,260-45,315 yuan per tonne and the LME/Shanghai copper arbitrage ratio was at 8, compared with 7.99 on Friday. The ratio was around 7.88 before the Lunar New Year holiday.

Precious metals

Precious metals were firmer this morning. The spot gold price was little changed at $1,571.38 per oz, but that was up from $1,565.58 per oz at a similar time on Friday morning. Silver prices were also little changed at $17.73 per oz, while platinum and palladium were up by 1.1% and 0.8%, respectively.

Wider markets

The yield on benchmark United States 10-year treasuries has weakened and was recently quoted at 1.59%, compared with 1.63% at a similar time on Friday. The German 10-year bund yield was slightly weaker too and was recently quoted at -0.39%, compared with -0.37% at a similar time on Friday.

Asian equities were for the most part weaker this morning – with the Nikkei down 0.6%, the Kospi down 0.49%, the ASX 200 down 0.14% and the Hang Seng down by 0.56%), while China’s CSI 300 was down by 0.27%.

Currencies

The dollar index (98.63) is holding in high ground, but other major currencies are mixed, with the yen (at 109.83) firmer on the back of haven interest, the Australian dollar (0.6705) is also firmer, while sterling (1.2901) and the euro (1.0954) are weaker.

Key data

Economic data already out shows China’s consumer prices index rose 5.4% against an expected rise of 4.9%. The index has been climbing at a fast pace since February last year when it troughed at 1.5%. China’s producer price index climbed 0.1%, this after being negative since August last year. Japan’s economy watchers sentiment index climbed to 41.9, from 39.8 previously. Later there is data on Italian industrial production and EU Sentix Investor confidence.

In addition, Federal Open Market Committee members Michelle Bowman and Patrick Harker are speaking.

Today’s key themes and views

For now, concerns about supply disruptions from China seem to be lifting base metals prices on the LME, while weaker prices on SHFE seem to be reflecting the likely demand situation in China. Overall, the combination of China being a net importer of most base metals and with the country facing a negative demand shock, it would not be unreasonable to expect prices to be weaker, but this might already have been priced-in, given the price weakness seen in the second half of January.

We expect choppy trading in the days and weeks ahead, until more is known about how big the demand shock will be.

Gold prices are edging higher and are likely to continue to do so until more is known about when the Wuhan coronavirus will be brought under control. Prices might well have been rising at a faster pace were it not for the stronger dollar and generally strong equity markets.

Published onFebruary 10, 2020 09:08 AM By William Adams

David