Economists, experts, and market participants await Friday’s Core PCE report

The financial markets are currently in the process of factoring in or getting in front of the upcoming release of the core PCE (Personal Consumption Expenditures) report. On Friday the Bureau of Economic Analysis (BEA) will release the most current information on inflation for December. Current estimates are anticipating a continued decline in core inflation from 4.7% in November to 4.4% (year-over-year) last month.

This is welcome news to Americans, but more importantly, is the last critical economic report that the Federal Reserve will have available as it convenes to decide the pace and size of upcoming interest rate hikes. Although Federal Reserve members have expressed mixed messages regarding their opinion on the pace of upcoming rate hikes as well as their upside target to take their benchmark “fed funds” rate to. It is currently widely accepted that the Fed will raise rates by ¼%, the first small rate hike since their first rate hike in March of last year.

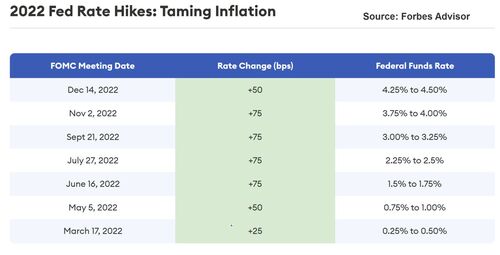

The Federal Reserve had maintained rates between 0 and ¼% since 2018. That ended in March 2022 when the Federal Reserve raise rates by ¼%. What followed a series of extremely aggressive rate hikes of ½ a percent in May. Followed by four consecutive ¾% hikes in June, July, September, and November. Finally, in December they only raise rates by half a percent. Collectively the seven consecutive rate hikes took interest rates from near zero to between 4 ¼ and 4 ½%.

It is widely expected that the Federal Reserve will slow the pace of rate hikes with a ¼% rate hike during the January FOMC meeting. The CME’s FedWatch tool currently is forecasting that there is a 99.7% probability that the Fed will raise rates by only ¼% and a 0.3% probability that the Fed will raise rates by ½ %. The Federal Reserve is also on record according to their most recent economic projections released in December of last year that they expect to take their benchmark rate just above 5% and not reduce that level for the entire year and possibly into the first or second quarter 0f 2024.

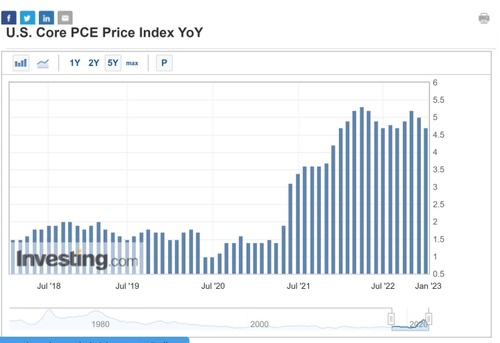

.jpg)

According to Investing.com the US core PCE index was at 4.7% (year-over-year) in November and is expected to decline to 4.4% in December. This clearly illustrates that the Federal Reserve’s aggressive monetary policy has effectively decreased inflation during 2022. However, the Federal Reserve’s most recent economic which was released at the December FOMC meeting clearly stated that they do not intend to reduce interest rates during the entire calendar year of 2023.

The Federal Reserve was slow to act and made a stupendous blunder by not raising rates until March 2022. This is when headline inflation was at 8.5%. Considering that headline inflation was at 2.6% exactly one year earlier the decision to not raise rates was one of the worst calculations by any Federal Reserve in history. However, the aggressive rate hikes implemented by the Fed last year although extremely painful were correct and did reduce inflation dramatically.

The question now is whether or not the Federal Reserve will back away from its stance of maintaining interest rates at this elevated level throughout the year, or once again become data-dependent and reposition its policy based upon this new data that they have effectively put a dent in inflation.

By Gary Wagner

Contributing to kitco.com

David